What Is A Credit Score?

You’ve heard that a credit score is important, haven’t you? You may have even heard how you should protect your credit score. But a lot of people are still unsure of what a credit score actually is.

Let’s take a look at credit scores and what they mean. This way you know once and for all what they are and how they are used.

A credit score is a calculation based on information from a credit report which gives a representation of how credit-worthy a person is or how likely a person is to default on their loan.

Let’s take a quick step back, shall we? We’re talking about credit scores but it’s important to understand what a credit report is all well. Your credit report is basically a listing of all the credit accounts you have and your history paying your credit, or debt, off. Sometimes the report is referred to as your credit history. The information comes from the lenders who report your activity to the three major credit bureaus.

To quickly sum up — your credit report gives information and a history of your credit accounts. Now back to credit scores…

Your credit score gives a number range to quickly sum up the information from your credit report.

Think of it like this — your credit score is like your GPA (Grade Point Average) for your credit use. A high GPA means you’re a pretty good student and a low one means you could be doing better. When you hear that someone has a 3.9 GPA you think “wow that’s a smart guy who studies hard.” A high credit score is similar. An excellent score shows lenders that you’re good with your credit and you pay on time — you’re basically not much of a risk.

Think of it like this — your credit score is like your GPA (Grade Point Average) for your credit use. A high GPA means you’re a pretty good student and a low one means you could be doing better. When you hear that someone has a 3.9 GPA you think “wow that’s a smart guy who studies hard.” A high credit score is similar. An excellent score shows lenders that you’re good with your credit and you pay on time — you’re basically not much of a risk.

On the other end of the spectrum a low credit score tells a lender you could be doing better with your credit and they see you as a bigger risk when lending you money or giving you credit (like on a credit card account).

The most common credit score is the FICO score which calculates based on reports from the agencies Experian, Equifax, and TransUnion. Be aware there are a good number of different variations of credit scores used by lenders, some depending on the field they cover like auto loans or mortgages. But the basic one is the standard FICO that you or I can check.

Why Your Credit Score Is Important

When you apply for a loan, be it for a car, house, or credit card, the lender will look at your credit score to measure what kind of interest rate to charge you.

The higher your score the lower your rate. The lower your score the higher your rate.

It’s in your best interest to have a better score as the interest rate charged is basically how much you will be paying to borrow money. A high score means you are more likely to pay back the loan without problems. A low score means there’s considerable risk in giving you a loan so a lender will charge you more for a loan in case you don’t pay it back.

(See my article Buying A Car – Know Your Credit Score And Get Financing Before Hand for an example of how knowing your credit score can help you save money).

Credit scores are becoming more and more important.

They are being used in job interviews (to see if the applicant is responsible with his credit), for insurance rates, and even to get cell phone contracts.

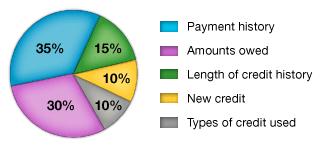

How Is Your Credit Score Determined?

The score is calculated approximately by:

The score is calculated approximately by:

- 35% Payment History – How well you have paid and if they have been on time

- 30% Credit Owed – The amount you owe relative to the amount of credit you have available

- 15% Length of Credit History – How old your oldest account is and the average age of your credit

- 10% New Credit – Amount of credit opened recently as well as recent credit inquiries

- 10% Type of Credit in Use – The mix of credit cards, retail accounts, finance loans, and mortgage loans.

For more details check out: Factors of a Credit Score

Understand though that your credit score is only measuring your credit accounts. If you pay cash for everything that activity won’t show up as part of your credit score. Your income is also not part of your score. So if you make a lot and pay for cash all the time you can actually have a low credit score.

What Do The Credit Score Ranges Represent?

The FICO score ranges from 300 to 850. It’s graded as such:

| 300-550 | Poor | May be rejected, or only accepted for very high interest rates |

| 551-650 | Average | Qualify for high interest rates |

| 651-710 | Good | Qualify for moderate rates |

| 711-750 | Very Good | Qualify for very competitive rates |

| 751 and up | Excellent | Lowest interest rates |

Be aware these ranges can change but they give you a good approximation of what to expect.

How To Make Your Credit Score Better

Here are a few tips to improve your credit score:

- Pay your bills on time and make it an ongoing habit.

- Pay off your debt. Don’t just move it around.

- Don’t max out your credit.

- Request credit reports from the three main agencies and check for any errors that may show. They are not all identical and one could have an error or even fraud.

- Avoid opening a number of new accounts in a short period of time.

When Do You Need Your Credit Score?

If you are planning on getting financing for a car or a home you should request the three credit reports and your credit score. Car insurance companies also use your credit score to help determine how much to charge you.

Remember, credit reports only list information about your accounts while the credit score is the interpretation of your accounts. You should have both.

Click here to see how you could possibly get your credit score free.

Your credit score is an important financial number that, if kept high, can potentially save you thousands of dollars over time.

Good explanation! Funny, I never thought about my credit score until I needed a mortgage. I just acted responsibly and it took care of itself. There usually no surprises unless someone made a mistake.

Use credit wisely and pay your bills on time and you have an easy road to a great credit score.

I lot of people know what their scores are and why its important be never really know what it is and how to improve. Well I guess people should know paying your bills on time that would be a given. But the making sure the balance is low and having different types of credit and the age of the credit seem foreign to many. I like the credit score is like a GPA.

If really not too difficult to keep your score good (well, except that you have to pay your bills). Knowing the factors can go a long way to maintaining an excellent credit score. And like you say, a low debt to credit ratio and keeping your oldest credit are a couple of things people may not know about.

I’m really on the fence about employers checking employee credit scores. It just seems like an invasion of privacy. I understand that credit reports can show potential risks to an employer about someone, but I still am not 100% OK with it.

As a small business owner, I would not want to see the credit report of someone I was hiring. I feel like that is their private business.

Just curious, what are your thoughts on it?

For the most part I do agree with you. What someone does, or doesn’t do, with their finances is their business and doesn’t necessarily reflect on their work ethic. I can see some logic to it if your job involves handling money in some fashion.

I’d love to hear arguments from an employer on why it’s a good thing to check a credit score before hiring. I’m certainly open to hearing about it.